Why gold is more than a safe haven for central banks

Our 2025 Central Bank Gold Reserves Survey shows strong indications that gold will remain a key reserve asset over the next 12 months. 95% of reserve managers surveyed expect central banks to continue increasing their gold reserves, while 43% actively plan to increase their own gold holdings.

The survey recorded record levels in terms of both buying sentiment and survey participation, with 73 central banks interviewed representing half of the global central banking community—the highest level of engagement since the survey began eight years ago.

This paints a bullish picture for central banks, which account for 20% of annual physical gold demand and have been net buyers for 15 years. Purchases exceeded 1,000 tonnes for the third consecutive year, well above the average of 400–500 tonnes recorded by central banks in the previous decade.

With the vast majority expecting buying momentum to continue and most seeing the US dollar becoming a smaller percentage of global reserve assets, we believe the survey further affirms gold’s status as a strategically important asset supporting the stability of the financial system.

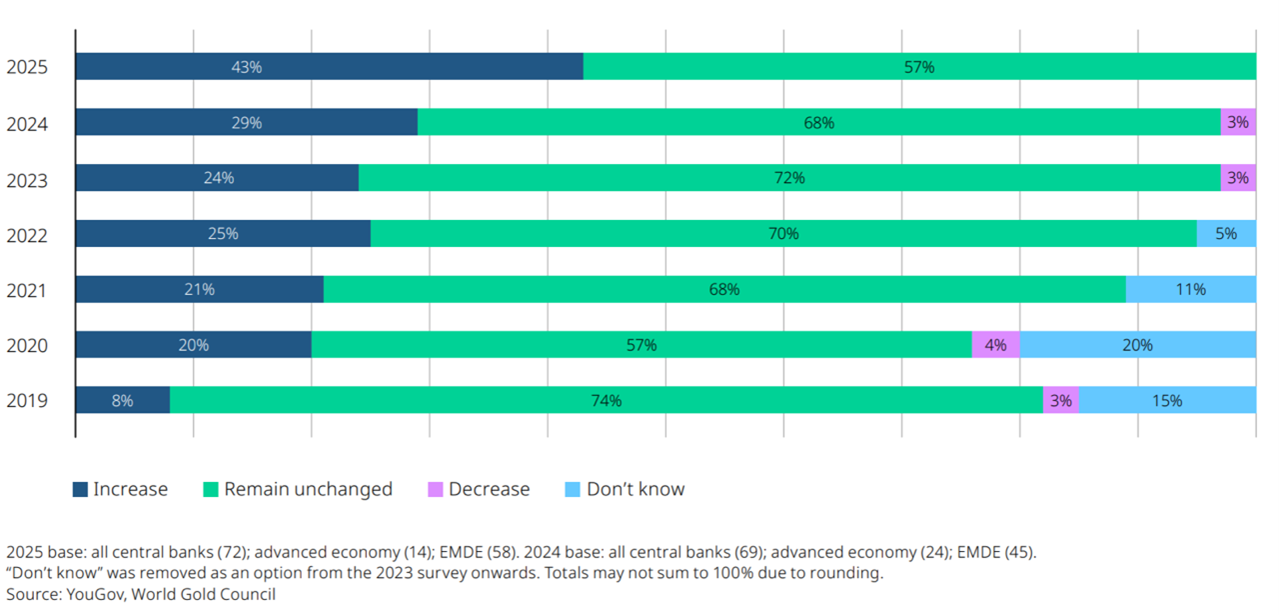

Chart 1: How do you expect your institution’s gold reserves to change over the next 12 months?

No surveyed central bank plans to reduce its exposure to gold

Conducted between February and May of this year, the survey reveals an increasingly unified view among central bankers: gold is not just a safe haven, but a strategic cornerstone. The 43% of reserve managers planning to increase their gold reserves over the next 12 months is up from 29% last year and, notably, no surveyed central bank plans to reduce its exposure to gold.

Unsurprisingly, the macroeconomic environment is a major factor behind gold’s appeal. When asked which issues are most relevant for reserve management, 93% of respondents cited interest rate levels, inflation, and geopolitical instability. Potential trade conflicts and tariffs, newly introduced as a survey category this year, ranked fourth overall and were a source of greater concern for EMDEs (69%) than for advanced economies (40%).

The conviction for gold is particularly pronounced among central banks in emerging markets and developing economies (EMDEs). Nearly half of EMDE respondents plan to increase their gold reserves, compared to a more conservative stance from developed markets. Geopolitical hedging and portfolio diversification are top priorities for EMDE reserve managers.

Chart 2: Which topics are relevant to your reserve management decisions?

Interestingly, advanced economies rank ESG issues as the third most important consideration for reserve management decisions, on par with inflation, after interest rates. Given the strong rate of purchasing, this indicates a high level of comfort with gold’s ESG footprint and the gold sector’s commitment to responsible mining and distribution.

Why do central banks prefer gold?

Three key factors for central bank gold purchases:

- gold’s historical performance during periods of crisis;

- its effectiveness as a diversifier and long-term store of value; and

- its role as a store of value serving as a hedge against inflation.

85% of respondents cited gold’s historical performance during economic downturns as a key reason for their reserve allocation decisions. 81% stated that diversification benefits it, and 80% pointed to its role as a store of value.

The survey found growing disillusionment with traditional reserve currencies, which is driving gold held domestically in local currencies. While the US dollar still dominates global reserve portfolios, 73% of central banks now expect a moderate or significant reduction in USD reserves over the next five years. At the same time, respondents expect an increase in allocations to the euro, the renminbi, and gold, signaling a slow but steady shift in central bank portfolio allocation.

One respondent noted that while the US dollar remains deeply entrenched due to the strength of its financial markets and legal institutions, “protectionist measures such as tariffs are pushing reserve managers toward diversification,” especially in politically non-aligned nations.

Active gold management increases

The survey also found a notable increase in the number of central banks actively managing their gold reserves, rising to 44% this year from 37% in 2024—another new high since we began collecting this data.

While yield enhancement remains the primary objective, mainly through gold lending and swaps, risk management has overtaken tactical trading as the second most cited reason for active management. This highlights gold’s evolving role as a stabilizer within the broader portfolio.

Interestingly, 75% of central banks continue to manage gold reserves separately from other assets, compared to 67% in 2024. When asked why, most respondents emphasized gold’s strategic importance and different accounting treatments. Among advanced economies, its status as historical legacy is another key reason.

Chart 3: How relevant are the following factors in your organization’s decision to hold gold?

Shifts in custody and storage

There is also an ongoing geographical shift in how and where gold is stored. While the Bank of England remains the preferred storage location (selected by 64% of respondents), the share of central banks using domestic storage jumped to 59% this year from 41% in 2024. However, only 7% plan to further increase domestic storage in the coming year, suggesting that the current level of national reserves may be near a peak.

Good Delivery bars are the preferred option when buying and holding physical gold.

Interestingly, the percentage of respondents who prefer not to disclose their vaulting arrangements has decreased sharply, indicating a broader trend toward transparency in reserve management practices.

Gold affirms its place in a multipolar world

Central banks are not only increasing their gold allocations but are also becoming more strategic and intentional about how and why they hold gold, reaffirming a trend that has been underway for nearly a decade.

The ongoing shift away from the US dollar, the drive to protect against rising political and economic risks, and the commitment to building more resilient reserve portfolios all point toward gold.

As one central bank respondent put it:

“The uncertainty and volatility occurring in the markets are driving investors and central banks to increase gold investments to protect themselves against these unpredictable conditions.“

Gold’s role as a neutral, liquid, and resilient reserve asset that carries no third-party liability appears more vital in a multipolar financial landscape that continues to challenge traditional assumptions about currency stability, sovereign credit, and global trade.